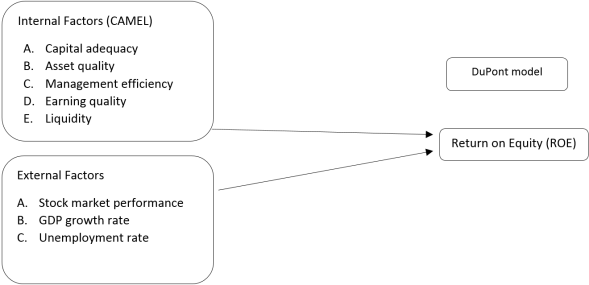

Using a random effects panel regression model, this study looks at how bank-specific and macroeconomic factors affect the financial performance of commercial banks, as measured by return on equity (ROE). The results, which are based on 105 observations from 21 banks, show that capital adequacy, management efficiency, and liquidity quality all have a positive and statistically significant effect on ROE. Management efficiency is the most important factor, which shows how crucial useful management is for making banks more profitable. But the quality of assets and earnings doesn't have significant impacts on ROE. The unemployment rate has an enormous detrimental impact on how well banks do, which means that bad job market conditions hurt their profits. Conversely, GDP growth and stock market performance exert no influence. The Breusch–Pagan test confirms the use of a panel model, and the Hausman test confirms that the random effects specification is appropriate. The model explains about 41% of the changes in ROE, which has substantial impacts on banking sector performance for both policy and managerial decisions. The research adds to the body of knowledge about banking and finance by giving real-world examples from a developing economy and giving useful information to bank managers, investors, and policymakers. Strengthening managerial effectiveness and optimizing capital structures can enhance profitability and resilience, particularly amid economic fluctuations and competitive market conditions.

| Published in | Journal of Finance and Accounting (Volume 14, Issue 2) |

| DOI | 10.11648/j.jfa.20261402.12 |

| Page(s) | 88-100 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

DuPont Analysis, Financial Performance, Bank Profitability, Capital Adequacy, Managerial Efficiency

Num | Variable type | Symbol | Variables | Measurement |

|---|---|---|---|---|

1 | Dependent variable | ROE | Return on equity* | Integrating net profit margin, asset turnover and equity multiplier |

2 | Independent variable | Cap_Ad | Capital adequacy ratio | Proportion of capital (Tier1 capital +Tier2 capital) to risk weighted asset |

3 | Asset_Q | Asset quality ratio | Proportion of non-performing assets to total loans or advances. | |

4 | Manege_E | Management efficiency ratio | Proportion of net income to total assets. | |

5 | Earn_Q | Earnings quality | Proportion of earning before interest and taxes to total capital employed.(Total equity +Long term liability) | |

6 | L_Qd | Liquidity ratio | Proportion of current asset to current liability | |

7 | GDP | Gdp growth rate | Annual growth of GDP | |

8 | St_Mp | Stock Market performance | Annual stock market capitalization index | |

9 | A_Une | Unemployment rate | Annual unemployment rate |

N | Minimum | Maximum | Mean | Std. Deviation | |

|---|---|---|---|---|---|

Capital Adequacy Ratio | 105 | .0492 | .179 | .137 | .0229 |

Asset Quality Ratio | 105 | .00012 | .147 | .0437 | .02022 |

Managerial Efficiency | 105 | .0002 | .019 | .0071 | .00369 |

Earnings Ratio | 105 | .0007 | .127 | .030 | .017 |

Liquidity Ratio | 105 | .670 | 2.00 | 1.1178 | .24018 |

GDP growth | 105 | .0345 | 0.07880 | 0.062 | .015 |

Annual Unemployment | 105 | .044 | .054 | .048 | .0042 |

Stock market performance | 105 | -.123 | . 403 | .167 | .193 |

ROE (Dupont Analysis) | 105 | .007 | .9803 | .1158 | .11265 |

Cap_Ad | Asset_Q | Manege_E | Earn_Q | Liquidity | GDP | Stock_MI | Unemp | |

|---|---|---|---|---|---|---|---|---|

Cap_Ad | 1 | |||||||

Asset_Q | .101 | 1 | ||||||

Manege_E | .483** | -.268** | 1 | |||||

Earn_Q | .391** | -.081* | .534** | 1 | ||||

L_Qd | -.416** | -.357** | -.129 | -.323** | 1 | |||

GDP | -.009 | .235* | .056 | .162 | -.035 | 1 | ||

St_Mp | -0.37 | -.185 | -.035 | -.194* | .044 | -0.409** | 1 | |

A_Une | -.031 | .352** | -.053 | -.104 | 0.083 | -.620** | .551** | 1 |

Variable | VIF | 1/VIF |

|---|---|---|

Capital Adequacy Ratio | 1.62 | 0.616 |

Asset Quality Ratio | 1.58 | 0.633 |

Managerial Efficiency | 1.87 | 0.533 |

Earnings Ratio | 1.67 | 0.600 |

Liquidity Ratio | 1.50 | 0.665 |

GDP growth | 1.69 | 0.5934 |

Annual Unemployment | 2.14 | 0.466 |

Stock market performance | 1.51 | 0.664 |

Model | Random effects |

|---|---|

Variables | ROE |

Cap_Ad | 1.055097* (1.89) |

Asset_Q | -.2271254 (-0.42) |

Manege_E | 12.79998*** (3.45) |

Earn_Q | .6866231 (1.03) |

L_Qd | .187841*** (3.65) |

GDP | .5314396 0.79 |

St_Mp | .0681894 (1.33) |

A_Une | -6.430881** (-2.30) |

Constant | -.0083178 (-0.04) |

Bruech_Pagan test | Chi=3.81 P=0.0255 |

Hausman Test | Chi=2.12 P= 0.9770 |

R-Square | 0.4078 |

Wald chi2 | 50.64 |

Observtion | 105 |

Group | 21 |

DSE | Dhaka Stock Exchange |

FE | Fixed Effects |

GMM | Generalized Method of Moments |

GDP | Gross Domestic Product |

IFRS | International Financial Reporting Standards |

NPL | Non-Performing Loan |

OLS | Ordinary Least Square |

RE | Random Effects |

ROE | Return on Equity |

ROA | Return on Assets |

SME | Small and Medium Enterprises |

| [1] | Abiodun, V., Adewole, A., n. d. Estimation of Regression Coefficients in the Presence of Multicollinearity. |

| [2] | Ahlam, S., Ali, B., n. d. The use of Dupont Model in the Analysis of the Company’s Performance : A Case Study. |

| [3] | Magoma, A., Mbwambo, H., Sallwa, A., & Mwasha, N. (2022). Financial Performance of Listed Commercial Banks in Tanzania: A CAMEL MODEL Approach. African journal of applied research, 8(1), 228-239. |

| [4] | Al-Homaidi, E. A., Tabash, M. I., Farhan, N. H. S., Almaqtari, F. A., McMillan, D., 2018. Bank-specific and macro-economic determinants of profitability of Indian commercial banks: A panel data approach. Cogent Econ. Finance 6, 1548072. |

| [5] | Ameur, I. G. B., Mhiri, S. M., 2013. Explanatory Factors of Bank Performance Evidence from Tunisia 2. |

| [6] | Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008). Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions & Money, 18(2), 121–136. |

| [7] | Bahadori, M., Talebnia, G., Imani, Z., 2020. A Study of the Financial Soundness of Banks in the Framework of CAMEL model (Capital, Assets, Management, Earnings and Liquidity): The Case Study of Commercial and Non- Commercial Banks in Iran. |

| [8] | Bateni, L., Vakilifard, H., Asghari, F., 2014. The Influential Factors on Capital Adequacy Ratio in Iranian Banks. Int. J. Econ. Finance 6, p108. |

| [9] | Berger, A. N., & Bouwman, C. H. S. (2013). How does capital affect bank performance during financial crises? Journal of Financial Economics, 109(1), 146–176. |

| [10] | Berger, A. N., & Humphrey, D. B. (1997). Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research, 98(2), 175–212. |

| [11] | Bhatti, M. A., Sadiq, M., Albarq, A. N., Juhari, A. S., n. d. Risk Management and Financial Performance of Banks: An Application of CAMEL Framework. |

| [12] | Bourke, P. (1989). Concentration and other determinants of bank profitability in Europe, North America and Australia. Journal of Banking & Finance, 13(1), 65–79. |

| [13] | Chowdhury, T. A., Ahmed, K., 2009. Performance Evaluation of Selected Private Commercial Banks in Bangladesh. Int. J. Bus. Manag. 4, p 86. |

| [14] | Claudia, A., Indrati, M., 2021. Analysis of Effect on Asset Return, Return on Equity, Earning Per Share, and Net Profit Margin on Share Price on Banking Company. J. Res. Soc. Sci. Econ. Manag. 1, 64–78. |

| [15] | Demirgüç-Kunt, A., & Huizinga, H. (1999). Determinants of commercial bank interest margins and profitability. World Bank Economic Review, 13(2), 379–408. |

| [16] | Dincer, H., Gencer, G., Orhan, N., Sahinbas, K., 2011. A Performance Evaluation of the Turkish Banking Sector after the Global Crisis via CAMELS Ratios. Procedia - Soc. Behav. Sci. 24, 1530–1545. |

| [17] | Ebenezer, A. M., Opubor, E. E., Enitan, O. O., 2025. DETERMINANTS OF CREDIT RISK IN THE NIGERIAN BANKING INDUSTRY 18. |

| [18] | Ebrahimi, S. K., Bahraminasab, A., Seyedi, F. S., 2017. The Impact of CAMEL Indexes on Profit Management in Banks 7. |

| [19] | Fani, K. A., Khan, V. J., Kumar, B., Pk, B. K., n. d. Impact of Internal and External Factors on Bank Performance in Pakistan. |

| [20] | Fatima, N., n. d. Capital Adequacy: A Financial Soundness Indicator for Banks. |

| [21] | Financial-Performance-Analysis-of-Manufacturing-sectors-in-Bangladesh-Using-DuPont-Model, n. d. |

| [22] | Firandra, P. M., 2024. The Relationship of Inflation, Interest Rates, and Investment Risk with Financial Performance 3. |

| [23] | García-Herrero, A., Gavilá, S., & Santabárbara, D. (2009). What explains the low profitability of Chinese banks? Journal of Banking & Finance, 33(11), 2080–2092. |

| [24] | Gazi, Md. A. I., Alam, Md. S., Hossain, G. M. A., Islam, S. N., Rahman, M. K., Nahiduzzaman, Md., Hossain, A. I., 2021. Determinants of Profitability in Banking Sector: Empirical Evidence from Bangladesh. Univers. J. Account. Finance 9, 1377–1386. |

| [25] | Gwachha, K. P., 2023. An Analysis of the Determinants of Bank Stability in the Banking Industry of Nepal. Khwopa J. 5, 196–210. |

| [26] | Işık, Ö. Shabir, M., Demir, G., Puska, A., Pamucar, D., 2025. A hybrid framework for assessing Pakistani commercial bank performance using multi-criteria decision-making. Financ. Innov. 11, 38. |

| [27] | Islam, H., Islam, Md. S., Saha, S., Tarin, T. I., Soumia, L., Parven, S., Rahman, K., 2024. Impact of Macroeconomic Factors on Performance of Banks in Bangladesh. J. Ekon. |

| [28] | Jaber, J. J., & Al-khawaldeh, A. A. (2014). The impact of internal and external factors on commercial bank profitability in Jordan. International Journal of Business and Management, 9(4), 22. |

| [29] | Jariah, A., Lukiana, N., 2023. Management of Financial Performance Based on Capital Structure, Liquidity Ratio, Coverage and Activity. Assets J. Ilm. Ilmu Akunt. Keuang. Dan Pajak 7, 1–7. |

| [30] | Johnston, M. P., n. d. Secondary Data Analysis: A Method of which the Time Has Come. |

| [31] | Kabir, R., Islam, S. M. R., Molla, M., Akter, S., n. d. Geological Importance of Bangladesh in Geopolitics. |

| [32] | Kristianti, R. A., n. d. Factors Affecting Bank Performance: Cases of Top 10 Biggest Government and Private Banks in Indonesia in 2004 - 2013. |

| [33] | Kumara, A. S., n. d. Researching with Secondary Data: A brief overview of possibilities and limitations from the viewpoint of social research. |

| [34] | Lalithchandra, B. N., Rajendhiran, D. N., n. d. Liquidity Ratio: An Important Financial Metrics. |

| [35] | Ll, P., E, V., Cm, W., J, K., Re, M., 2020. Use of secondary data analyses in research: Pros and Cons. J. Addict. Med. Ther. Sci. 058–060. |

| [36] | Mahmud, I., 2023. CAMEL Ratios and Market Profitability: A Study on Banking Sector in Bangladesh. J. Financ. Mark. Gov. 2, 111–125. |

| [37] | Maude, F. A., Dogarawa, A. B., 2016. A Critical Review of Empirical Studies on Assessing Bank Performance using CAMEL Framework. SSRN Electron. J. |

| [38] | Mirović, V., Kalaš, B., Milenković, N., Andrašić, J., Đaković, M., 2024. Modelling Profitability Determinants in the Banking Sector: The Case of the Eurozone. Mathematics 12, 897. |

| [39] | Mitra, G., Gupta, V., Gupta, G., 2023. Impact of macroeconomic factors on firm performance: Empirical evidence from India. Invest. Manag. Financ. Innov. 20, 1–12. |

| [40] | Muhmad, S. N., Hashim, H. A., n. d. Using The Camel Framework In Assessing Bank Performance In Malaysia. |

| [41] | NGUYEN, H. D. H., DANG, V. D., 2020. Bank-Specific Determinants of Loan Growth in Vietnam: Evidence from the CAMELS Approach. J. Asian Finance Econ. Bus. 7, 179–189. |

| [42] | O’Connell, M., 2023. Bank-specific, industry-specific and macroeconomic determinants of bank profitability: evidence from the UK. Stud. Econ. Finance 40, 155–174. |

| [43] | Otekunrin, A., Nwanji, T., Fagboro, D., Olowookere, J., Ibitoye, S., 2021. Performance of Firm and Board Attributes Nexus: Using Hausman Test Analysis. Int. J. Financ. Res. 12, 268. |

| [44] | Qureshi, A. S., Siddiqui, D. A., 2023. The Impact of the CAMEL Model on Banks’ Profitability. SSRN Electron. J. |

| [45] | Raof, N. A., Azman, N. S. M., Azmi, N. N. K., 2025. Modelling Economic Growth: Panel Data Approach 14. |

| [46] | Rashedul Azim, M., Nahar, S., 2021. Evaluation of Internal Factors Indicating Bank Profitability in Commercial Banks Bangladesh. Int. J. Sci. Res. IJSR 10, 443–450. |

| [47] | Rathnasiri, R. A., 2024. The Impact of Macroeconomic Stability on Commercial Bank Profitability: A Study of Sri Lanka. Int. J. Account. 4. |

| [48] | Rehman, Z.-, Khan, S. A., Khan, A., Rahman, A., 2018. Internal Factors, External Factors and Bank’s Profitability. Sarhad J. Manag. Sci. 4, 246–259. |

| [49] | Saad, N. M., Mita, A. F., 2025. Unemployment Issues and Dynamic Determinants for Business Economics Landscape in ASIAN Countries. WSEAS Trans. Bus. Econ. 22, 516–528. |

| [50] | Sengupta, K., n. d. FROM THE FMS ARCHIVES. |

| [51] | Siddiqua, A., Chowdhury, A. N. M. M. H., Chowdhury, A. S. Md. M. H., Mainuddin, Md., Rahman, Md. L., 2017. Impact of Internal Factors on the Profitability of Banks: A Case of Commercial Banks in Bangladesh. Asian Bus. Rev. 7. |

| [52] | Susanti, N., Herawati, S. D., 2019. The Affect of External and Internal Factors on Banking Profitability. Int. J. Innov. 6. |

| [53] | Budhathoki, P. B., Rai, C. K., Lamichhane, K. P., Bhattarai, G., Rai, A., (2020). The Impact of Liquidity, Leverage, and Total Size on Banks’ Profitability: Evidence from Nepalese Commercial Banks. J. Econ. Bus. 3(2) PP. 545-555. |

| [54] | Uzhegova, O., 2015. The Relative Importance of Internal Factors for Bank Performance in Developed and Emerging Economies. Mediterr. J. Soc. Sci. |

| [55] | Vintilă, G., Nenu, E. A., & Gherghina, Ş. C. (2014). Empirical research towards the factors influencing corporate financial performance on the Bucharest stock exchange. Analele stiintifice ale Universitatii “Al. I. Cuza” din Iasi. Stiinte economice/Scientific Annals of the" Al. I. Cuza", 61(2). |

| [56] | Vodová, P. (2011). Liquidity of Czech commercial banks and its determinants. International Journal of Mathematical Models and Methods in Applied Sciences, 5(6), 1060–1067. |

| [57] | Zubair, Z. A., Aladejare, S. A., n. d. Exchange Rate Volatility and Stock Market Performance in Nigeria. |

APA Style

Hossain, M. S., Syan, M. K., Banu, M. H., Saha, S., Mia, M., et al. (2026). Assessing Bank Success Factors in Bangladesh Through the DuPont Model. Journal of Finance and Accounting, 14(2), 88-100. https://doi.org/10.11648/j.jfa.20261402.12

ACS Style

Hossain, M. S.; Syan, M. K.; Banu, M. H.; Saha, S.; Mia, M., et al. Assessing Bank Success Factors in Bangladesh Through the DuPont Model. J. Finance Account. 2026, 14(2), 88-100. doi: 10.11648/j.jfa.20261402.12

AMA Style

Hossain MS, Syan MK, Banu MH, Saha S, Mia M, et al. Assessing Bank Success Factors in Bangladesh Through the DuPont Model. J Finance Account. 2026;14(2):88-100. doi: 10.11648/j.jfa.20261402.12

@article{10.11648/j.jfa.20261402.12,

author = {Md. Sumon Hossain and Meharab Khan Syan and Mst. Hasna Banu and Sumi Saha and Masum Mia and Raj Kumar Moulick},

title = {Assessing Bank Success Factors in Bangladesh Through the DuPont Model},

journal = {Journal of Finance and Accounting},

volume = {14},

number = {2},

pages = {88-100},

doi = {10.11648/j.jfa.20261402.12},

url = {https://doi.org/10.11648/j.jfa.20261402.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jfa.20261402.12},

abstract = {Using a random effects panel regression model, this study looks at how bank-specific and macroeconomic factors affect the financial performance of commercial banks, as measured by return on equity (ROE). The results, which are based on 105 observations from 21 banks, show that capital adequacy, management efficiency, and liquidity quality all have a positive and statistically significant effect on ROE. Management efficiency is the most important factor, which shows how crucial useful management is for making banks more profitable. But the quality of assets and earnings doesn't have significant impacts on ROE. The unemployment rate has an enormous detrimental impact on how well banks do, which means that bad job market conditions hurt their profits. Conversely, GDP growth and stock market performance exert no influence. The Breusch–Pagan test confirms the use of a panel model, and the Hausman test confirms that the random effects specification is appropriate. The model explains about 41% of the changes in ROE, which has substantial impacts on banking sector performance for both policy and managerial decisions. The research adds to the body of knowledge about banking and finance by giving real-world examples from a developing economy and giving useful information to bank managers, investors, and policymakers. Strengthening managerial effectiveness and optimizing capital structures can enhance profitability and resilience, particularly amid economic fluctuations and competitive market conditions.},

year = {2026}

}

TY - JOUR T1 - Assessing Bank Success Factors in Bangladesh Through the DuPont Model AU - Md. Sumon Hossain AU - Meharab Khan Syan AU - Mst. Hasna Banu AU - Sumi Saha AU - Masum Mia AU - Raj Kumar Moulick Y1 - 2026/03/30 PY - 2026 N1 - https://doi.org/10.11648/j.jfa.20261402.12 DO - 10.11648/j.jfa.20261402.12 T2 - Journal of Finance and Accounting JF - Journal of Finance and Accounting JO - Journal of Finance and Accounting SP - 88 EP - 100 PB - Science Publishing Group SN - 2330-7323 UR - https://doi.org/10.11648/j.jfa.20261402.12 AB - Using a random effects panel regression model, this study looks at how bank-specific and macroeconomic factors affect the financial performance of commercial banks, as measured by return on equity (ROE). The results, which are based on 105 observations from 21 banks, show that capital adequacy, management efficiency, and liquidity quality all have a positive and statistically significant effect on ROE. Management efficiency is the most important factor, which shows how crucial useful management is for making banks more profitable. But the quality of assets and earnings doesn't have significant impacts on ROE. The unemployment rate has an enormous detrimental impact on how well banks do, which means that bad job market conditions hurt their profits. Conversely, GDP growth and stock market performance exert no influence. The Breusch–Pagan test confirms the use of a panel model, and the Hausman test confirms that the random effects specification is appropriate. The model explains about 41% of the changes in ROE, which has substantial impacts on banking sector performance for both policy and managerial decisions. The research adds to the body of knowledge about banking and finance by giving real-world examples from a developing economy and giving useful information to bank managers, investors, and policymakers. Strengthening managerial effectiveness and optimizing capital structures can enhance profitability and resilience, particularly amid economic fluctuations and competitive market conditions. VL - 14 IS - 2 ER -

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh

Department of Accounting and Information Systems, University of Rajshahi, Rajshahi, Bangladesh